Executive Summary

Introduction

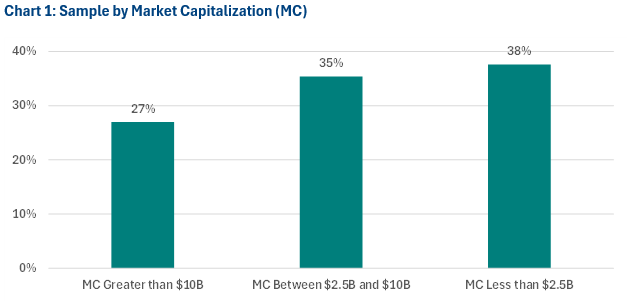

Southlea’s latest research report summarizes year-over-year director compensation trends among the companies within the S&P/TSX Composite Index. Data reflect 226 companies that disclosed compensation for their board of directors and have been summarized by company size in terms of market capitalization (MC), with a fairly well distributed group of companies in each size category. The data were collected by ESGAUGE, a data analytics firm.

Methodology

Data in this report reflect compensation disclosed in 2024, 2023, and 2022 proxy circulars representing 2023, 2022, and 2021 compensation levels, respectively. Total compensation is estimated based on a standard number of meetings and committee memberships (eight board meetings, two committee memberships and four committee meetings per committee) to provide an apples-to-apples comparison for similar workloads. All data are in the currency reported by each company and are summarized at par (e.g., $1CAD = $1USD). For comparison purposes, we have also provided data for the S&P 500 in USD. Each element is independently arrayed and cannot be added to form the total.

Board Member Compensation

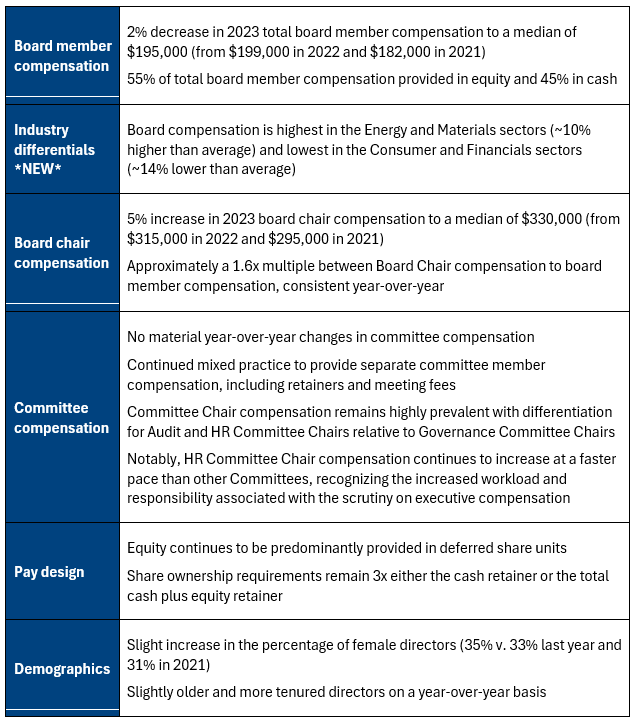

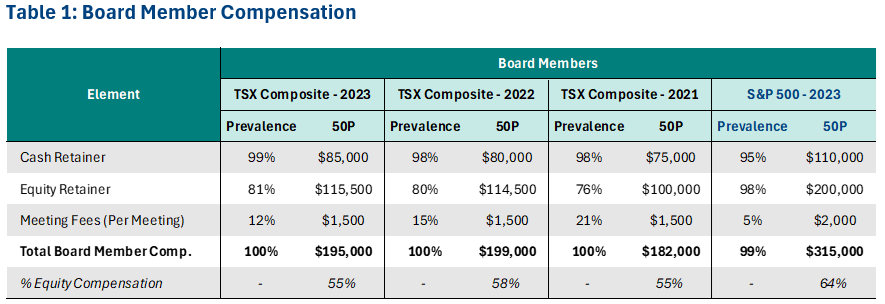

Total board member compensation for the TSX Composite fell slightly at the 50th percentile (median, or 50P) from $199,000 to $195,000 between 2022 and 2023; however, pay levels remain above those in 2021 ($182,000). The relative weight on compensation delivered in cash v. equity remains consistent at 55% weight on equity (cash includes the cash retainer and meeting fees where applicable).

In 2023, total board member compensation for the S&P 500 was $315,000 USD, approximately 60% percent higher than the TSX Composite, driven by a combination of higher pay levels and larger companies. We note that the difference is less for cash compensation with significantly higher equity retainers driving the overall total board member compensation difference.

The premium observed at median in the S&P 500 over the TSX Composite is higher in 2023 (v. 50% in 2022), demonstrating that pay levels increased in the U.S. while they have been flat in Canada. This increasing pay disparity could result in difficulties for Canadian companies to attract and retain North American / Global board members. This also raises questions on the inclusion of U.S.-based peer companies and how to address currency between Canadian and non-Canadian-based directors (e.g., residency-based pay).

Companies continue to move away from providing board meeting fees with 12% of companies (v. 15% last year and 21% the year before) continuing this practice, reflecting a persistent trend towards an “all-in” retainer structure.

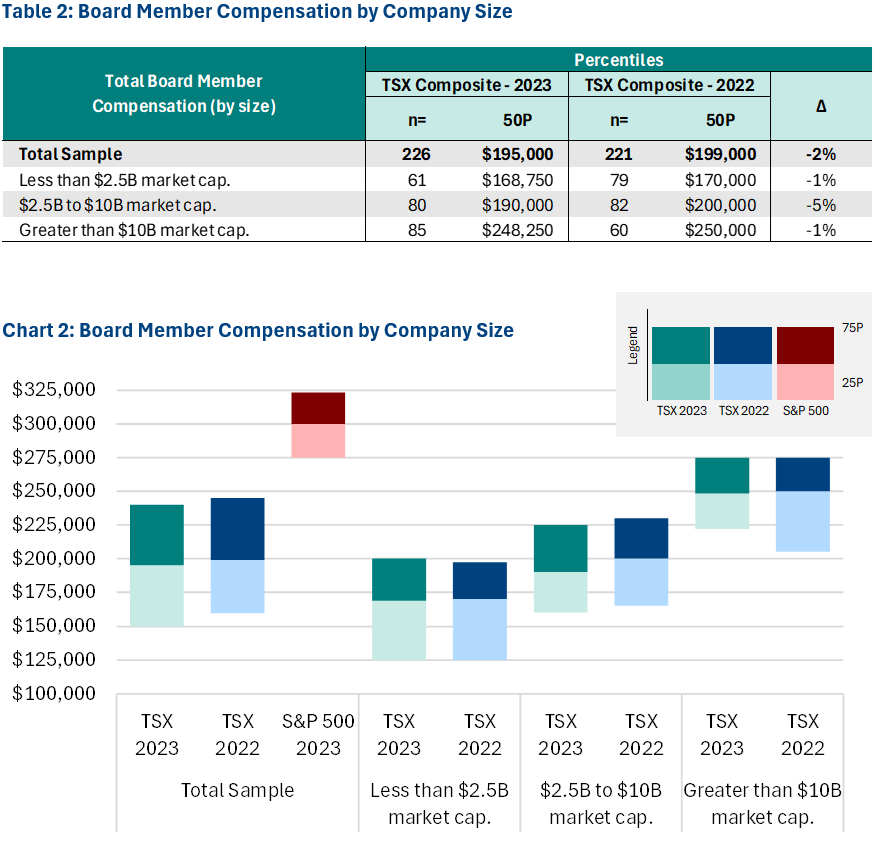

Board Member Compensation by Company Size

We observe a clear relationship between company size (in terms of market capitalization) and total board member compensation. Flat to slightly lower pay levels are consistent across the sample with an approximate 1% to 5% decrease year-over-year depending on the size of company. The range of compensation among companies of a similar size represents the diversity of practices depending on the organization’s scope, industry, and relative complexity.

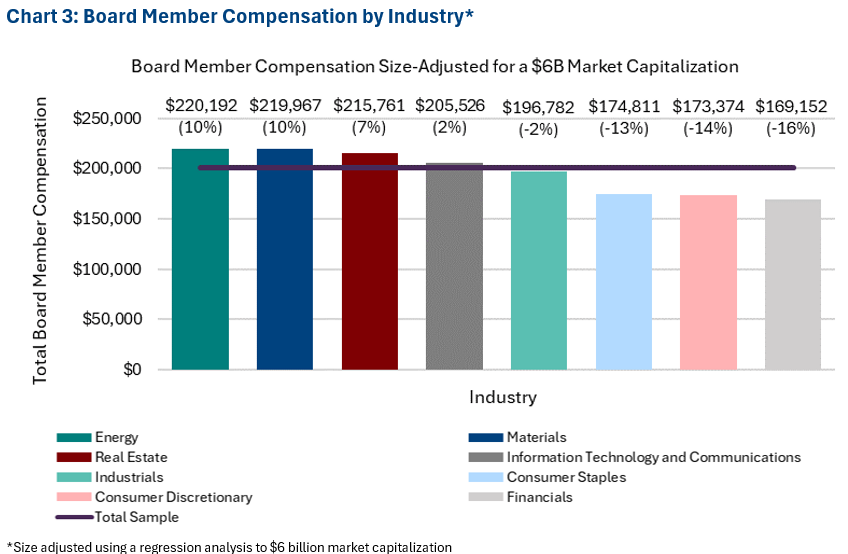

BOARD MEMBER COMPENSATION BY INDUSTRY

Board member compensation is highest in the Energy and Materials sectors and lowest in the Consumer and Financials sectors. We note that this summary has been normalized to reflect a company with a market capitalization of $6 billion to provide a clearer perspective of the industry impact on compensation. These industry differences may reflect the different talent markets required for each industry, e.g., some industries may have a broader global talent market, or require unique skills / experience, which puts upward pressure on compensation.

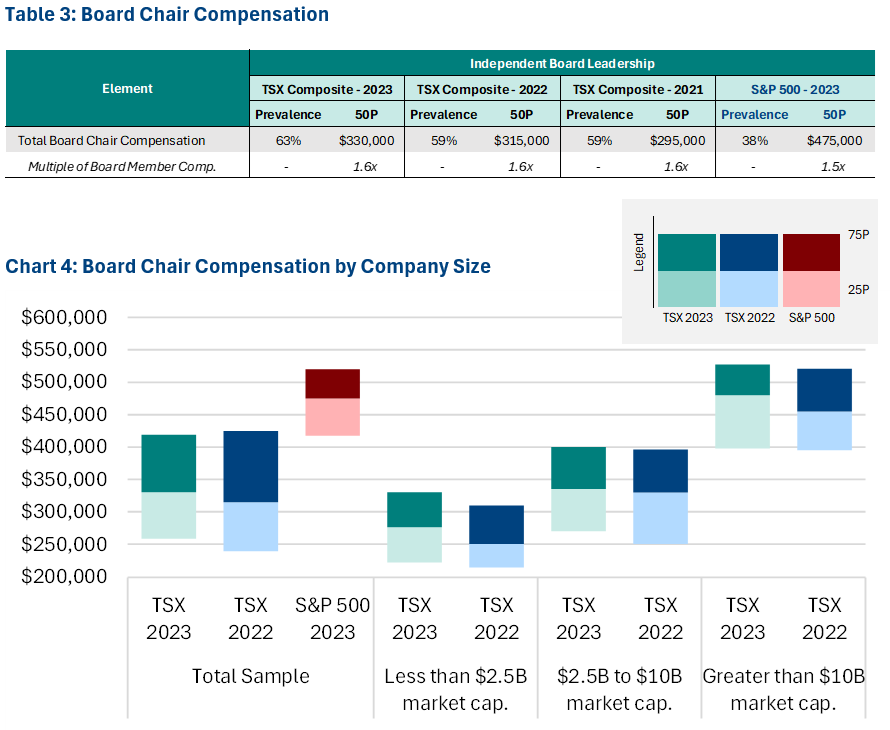

Board Chair Compensation

Of the 60% of TSX Composite companies with a non-executive Board Chair, total Board Chair compensation at the 50th percentile increased from $315,000 to $330,000, representing a 5% increase. When expressed as a multiple of board member compensation, Board Chair’s receive 1.6x board member compensation at the 50th percentile, consistent with the past two years.

In the U.S., approximately 40% of the S&P 500 have a non-executive Board Chair, reflecting the increased prevalence of a combined Board Chair and CEO. Non-executive Board Chair compensation is higher than in Canada at $475,000 and represents approximately the same multiple to board member compensation (1.5x) as found in Canada (1.6x).

Committee Compensation

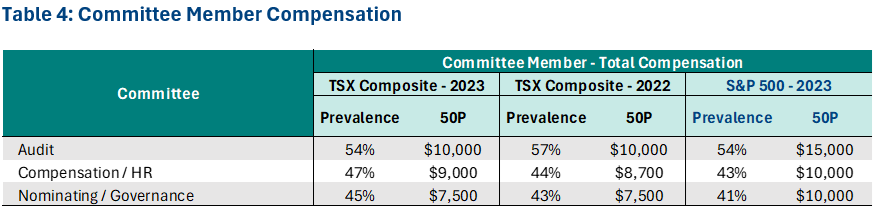

There is mixed usage of additional compensation (retainers and/or meeting fees) for committee member participation with a higher prevalence for Audit v. other committees. Total committee member compensation at the 50th percentile varies by committee at $10,000 for Audit, $9,000 for Compensation / HR and $7,500 for Nominating / Governance with no year-over-year change except for the Compensation / HR committee (up 3% year-over-year, following an 11% increase between 2021 and 2022). Committee member compensation in Canada remains lower than the S&P 500.

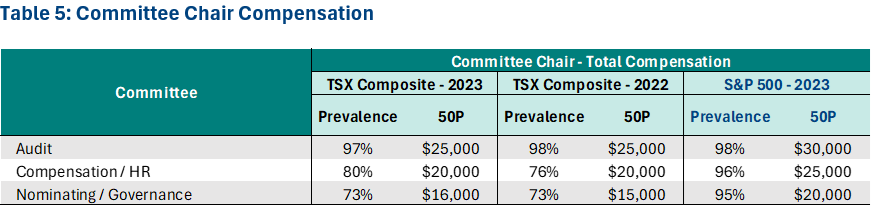

Additional compensation for Committee Chairs (including retainers and meeting fees) is more prevalent, particularly for Audit Committee Chairs. Total compensation at the 50th percentile varies by committee at $25,000 for Audit, $20,000 for Compensation / HR and $16,000 for Nominating / Governance influenced by the respective workloads of each committee. Committee Chair compensation remained relatively consistent year-over-year, with a 7% increase to Nominating / Governance Committee Chair compensation only. Pay levels remain slightly below the S&P 500.

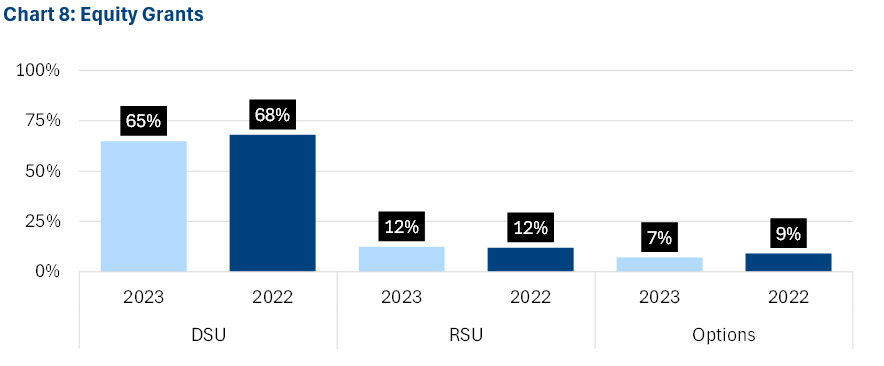

Board Equity Grants

The majority of TSX Composite companies continue to grant deferred share units (DSUs) with approximately 12% granting restricted share units (RSUs) and 7% granting stock options, with little change on a year-over-year basis. The use of stock options is typically in resource-based and/or recently public companies. In the U.S., S&P 500 companies grant equity primarily in RSUs.

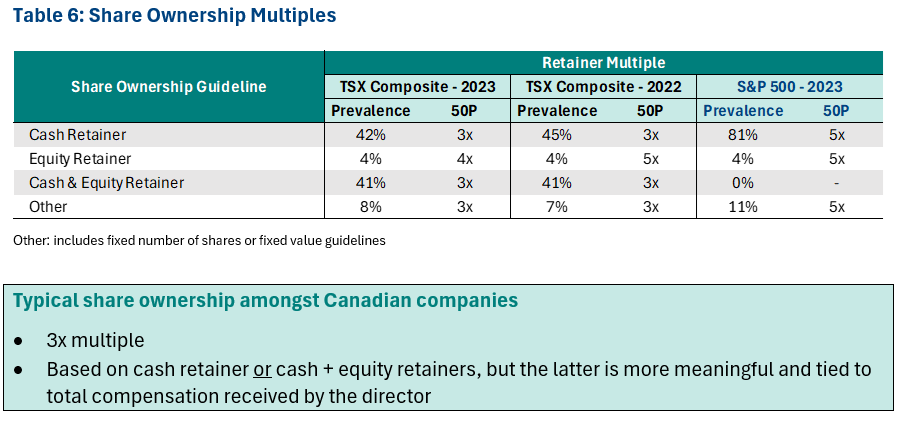

Share Ownership Requirements

Share ownership requirements are similar year-over-year. Almost all TSX Composite companies articulate share ownership requirements for board members as either a multiple of the cash retainer or cash + equity retainers. Despite the significantly different total dollar amounts resulting from the differing ownership definitions, the median multiples of both cash and cash + equity retainers are 3.0x.

Given recent preferences expressed by the Canadian Coalition for Good Governance in 2022 and the Globe & Mail Board Games in 2024 to define executive share ownership as a multiple of total direct compensation instead of salary, organizations wishing to comply may also re-evaluate their Board member ownership guidelines (in which total retainer is analogous to the notion of total compensation for executives).

In the U.S., most S&P 500 companies express the requirement as a multiple of the cash retainer. They also have a higher requirement at 5x the retainer (v. 3x in Canada) but that is on a relatively lower cash portion of the retainer whereas close to 40% of Canadian companies apply their requirement to the total of the cash + equity retainers.

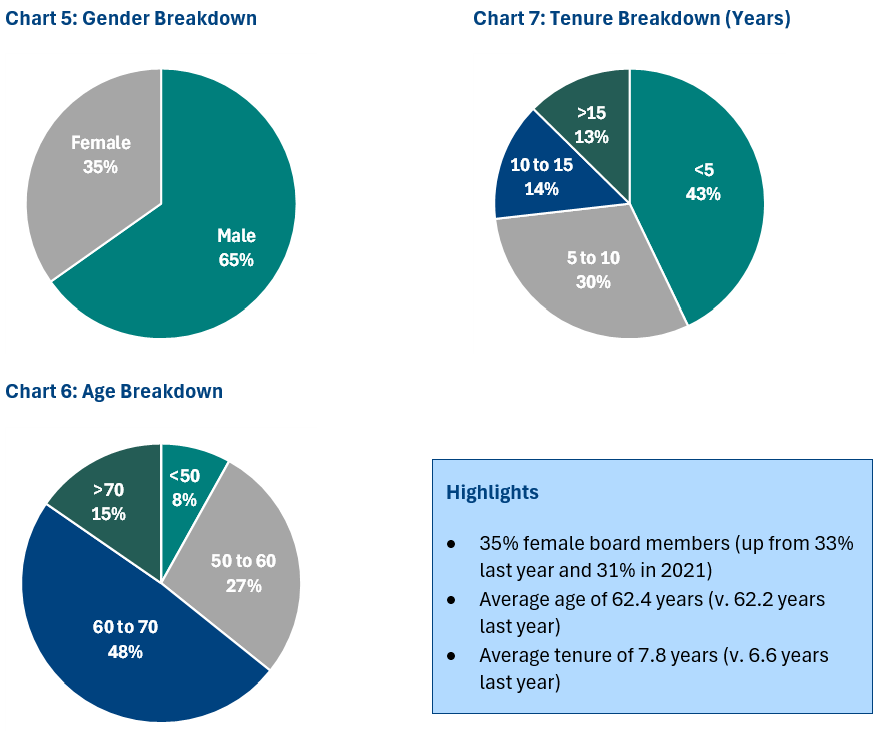

Board Demographics

TSX Composite companies tend to have between 7 to 13 board members with an average of 35% female board members (up from 33% last year and 31% in 2021). In terms of age, 35% of board members are less than 60 (down from 38% last year) with about one-half between age 60 and 70.

Board member tenure has increased year-over-year, with a lower proportion with less than a five-years tenure (43% this year v. 56% last year and 47% in 2021) and more board members serving on the board for greater than 10 years (27% this year v. 21% last year and 26% in 2021).

About The Authors

Ryan Resch, Senior Partner

Ryan is a founder and Senior Partner of Southlea, a GECN Group company. He has over 20 years of experience consulting complex organizations across North America on executive and broad-based compensation including related governance considerations. He is often the named executive compensation consultant representing either the human resources committee and/or management. Prior to forming Southlea, he worked in Willis Towers Watson’s Toronto and Vancouver offices leading many of the practice’s large client relationships.

He leverages this expertise to bring stakeholders together and drive meaningful change aligned with key business and talent priorities. He is known for providing fresh and innovative thinking with his most recent research focused on connecting environmental, social and governance (ESG) with people and pay programs.