2026 Changes to Board Games Methodology

In February, the Globe and Mail published Board Games Methodology for 2026. Board Games generally publishes an annual report assessing the governance practices and disclosures of the S&P/TSX Composite Index in early December.

Changes made to the 2026 Board Games criteria are minor, involving only an additive adjustment to Question 10 – Cybersecurity and Artificial Intelligence. Under the updated criteria, while full points remain at two, companies may earn one point if they describe how the board considers cybersecurity and technological risk issues but do not specifically mention artificial intelligence.

Top 5 Questions Issuers Lost Points in 2025 Board Games

In this blog, we also review the 2025 Board Games results and identify the top five compensation-related questions that the Composite Issuers lost points in the previous year:

Topic

Methodology

Southlea Comments

Q26. CEO Share-holding Periods

ONE mark if the company requires CEOs to hold shares for at least one year post-departure.

65% of the composite issuers received zero marks for this question. While the implementation of a post-retirement/employment holding period remains uncommon within the Canadian market, this percentage has marginally decreased from 2024.

Q30. Use of Adjusted Financial Metrics in Compensation

One mark if the company discloses adjustments to IFRS/GAAP earnings used in annual incentive plans and provides a reconciliation table linking the adjusted figure and the IFRS/GAAP figure in audited financial statements.

ONE mark if the company does not use adjusted metrics in the executive compensation plan. ZERO marks if the company uses adjusted IFRS/GAAP figures in the executive compensation plan without providing a reconciliation in the proxy circular.

53% of the composite issuers received zero marks for this question.

This disclosure is required under Glass Lewis’ Canadian benchmarking policy guidelines. The proxy advisor believes a detailed discussion of adjustments (i.e. IFRS/GAAP-to-non-IFRS/GAAP reconciliation) used for compensation purpose enables investors to evaluate the effectiveness of the incentive payout.

CCGG also pointed out in its 2025 Best Practices for Proxy Circular Disclosure two most material gaps between existing proxy circular disclosure and shareholder disclosure expectations:

• An explanation of parameters the board uses to assess adjustments to GAAP figures for compensation purposes, and • A plain language explanation of the board’s rationale for approving any material GAAP figures adjustments used in the compensation scheme in the most recently completed fiscal year.

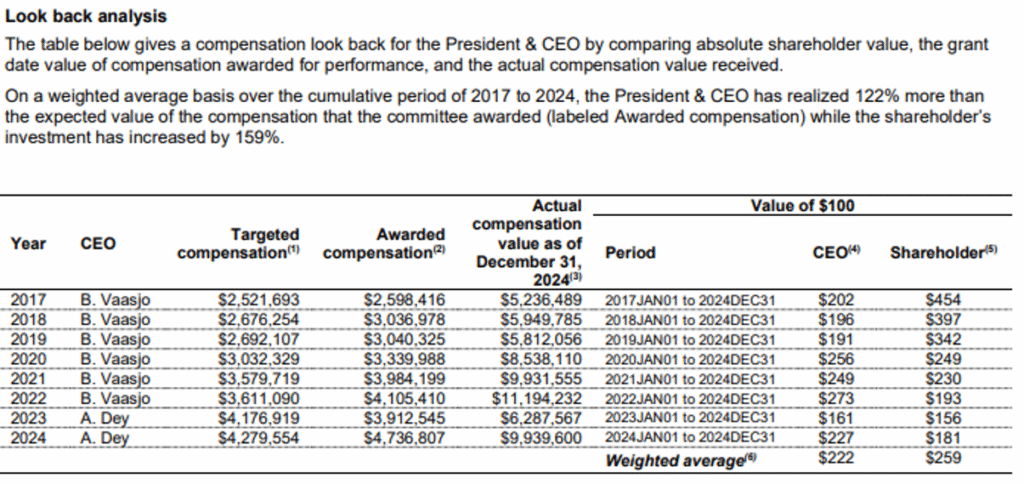

Q22. Historical Compensation Disclosure

ONE mark if the company provides a “look-back” table in the proxy circular showing CEO realized pay over last five years, including long term incentives. The table must show investors how the CEO’s actual pay compared to the reported pay.

ZERO marks if no information is provided or if it does not include all pay elements.

51% of the composite issuers received zero marks for this question.

To earn full points for this question, the chart should disclose all long-term compensation elements with an annual breakdown for each of the past five years, and clearly show actual payouts compared to intended compensation for each year.

This table – often referred to as a “realized pay” table – compares vested share units and exercised options to the granted amount and is typically presented alongside five-year investors returns.

See Appendix I for the 2025 best practice example highlighted by CCGG.

Q25. Compensation Clawbacks

ONE mark if the company’s clawback provision covers bonus payments to the CEO if wrongdoing is discovered. The policy must allow directors to claw back payments for anything the board determines to constitute wrongdoing.

ZERO marks if the company’s clawback policy applies only to financial statements restatements due to wrongdoing. ZERO marks if there is no clawback policy.

45% of the composite issuers received zero marks for this question.

CCGG, in its Executive and Director Compensation Guidebook, advocates for broad clawback policies that may be triggered by either a financial restatement or employee misconduct. Such policies should apply to all forms of incentive compensation, including cash bonus, RSUs, PSUs, and stock options.

Glass Lewis supports clawback policies that permit recovery from current and former executive officers following a financial restatement or a similar revision of performance indicators upon which awards were based. Such policies should also allow for the recoupment of variable incentive payments, both time-based and performance-based, in the event of:

– material misconduct,

– a material reputational failure,

material risk management failure, or

– a material operational failure,

where the consequences have not already been reflected in incentive payments and recovery is warranted.

For further discussion on clawback effectiveness, please refer to Southlea’s recent blog “Will your clawback work?”

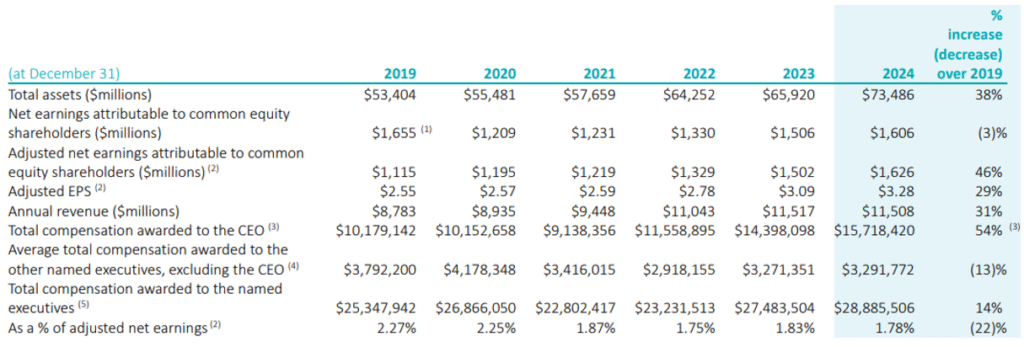

Q24. Cost of Compensation Comparisons

ONE mark if the company discloses the total compensation cost to the top executive team relative to a financial metric such as income or revenue. ZERO if it does not.

44% of the composite issuers received zero marks for this question.

Under Board Games’ methodology, comparing compensation cost to share price growth is insufficient, as the comparison must be made to the financial cost. The calculation should be presented as a percentage, not an approximation.

See Appendix II for an example that received the full mark for this question.

Appendix

I. “Look back analysis” table disclosed on pages 70-71 of Capital Power Corporation’s 2025 proxy circular

II. “Cost of management” table disclosed on page 68 of Fortis Inc.’s 2025 proxy circular

About The Author

Anqi Xu, Consultant

Anqi is a Consultant at Southlea Group and leads the Compensation Governance team.

Prior to joining Southlea Group, she worked as Associate Vice President at ISS, a global proxy advisory firm, producing independent shareholder meeting research reports with voting recommendations for institutional investors. She is also the Canadian research team’s E&S lead with in-depth expertise in the E&S shareholder proposal focus area.

Anqi also worked as Vice President at a leading Canadian strategic advisory firm, advising boards and committees on complex corporate governance matters, including proxy contests and M&As. She provided strategic guidance to public issuers on executive compensation and played a key role in multiple successful Say on Pay turnarounds.

Anqi has experience evaluating executive compensation structures and supporting effective disclosures for public-traded companies, the S&P/TSX Composite Index issuers in particular, across a range of sectors.

Anqi has a Bachelor of Arts in Economics and Art History from the University of California, Los Angeles (UCLA) and a Master of Financial Accountability degree from York University. She also holds a Chartered Financial Analyst (CFA) designation.