The CEO pay ratio disclosure requirement was first introduced by the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010. In 2015, the Securities and Exchange Commission (SEC) finalized the rule that requires US public companies to disclose their CEO pay ratio, defined as “the ratio of the compensation of its chief executive officer (CEO) to the median compensation of its employees”. In the UK similar disclosure requirements exist, with UK-listed companies with over 250 employees required to disclose CEO pay compared to the 25th percentile, median, and 75th percentile of employee pay.

Currently, Canadian regulations do not mandate the disclosure of CEO pay ratios. While certain companies have faced shareholder pressure to report CEO pay ratios or other vertical benchmarking metrics, widespread adoption has not occurred. The majority of organizations continue to prioritize horizontal benchmarking against peer companies, consistent with standard industry practice.

Considering Two Sides

The Rationale

Pressure from stakeholders. There may be external pressure from investors, the government, activist organizations, and the public to publish the CEO pay ratio. It could also be raised as part of union negotiations.

Demonstrates commitment to fair pay. When disclosed, the CEO pay ratio may indicate to shareholders, employees, and other stakeholders that the company is committed to fair pay, particularly in Canada where this disclosure is voluntary.

Additional lens through which to review CEO pay. The CEO pay ratio or broader vertical benchmarking (e.g., CEO to NEO pay) can be used as another tool in the Human Resources Committee’s (HRC) toolkit to monitor the trending of CEO pay relative to executive and broader employee pay levels.

The Challenges

Administratively burdensome. The cost to collect, validate data, and determine the appropriate calculation methodology can be time consuming, particularly when required to comply with disclosure rules. This is especially true for organizations that operate across multiple geographies (e.g., approach to currency, differing cost of living by region, etc.) and for organizations with different employee types (e.g., salaried vs. hourly, part-time employees, seasonal workers, independent contractors, etc.). While this is true when preparing the CEO ratio for disclosure purposes, if intended to be used as an internal metric, there are approaches to simplify the analysis.

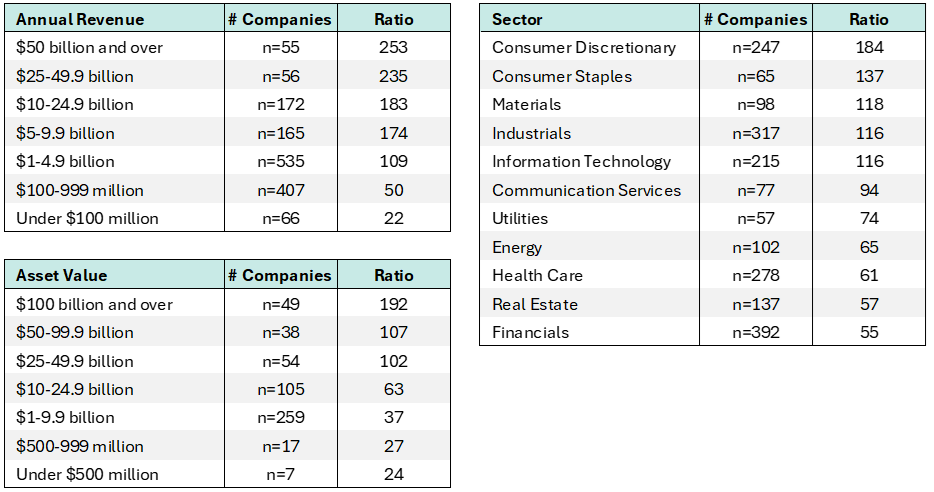

Challenging to interpret. CEO pay ratios vary widely by region, company size, and industry sector (refer to Table 1 below based on data collected by ESGAUGE, a data analytics firm). We have found that ratios vary widely, even within similarly sized organizations in the same industry, given differing methodologies applied and varying organization structures. This makes it challenging to compare externally.

Limited external benchmarks. Despite almost 10 years of disclosure, we have yet to see governance influencers converge around an acceptable CEO pay ratio, likely given the challenges with comparing across companies. In the absence of a clear benchmark for what constitutes an acceptable pay ratio, management faces challenges in interpreting the company’s figure and effectively communicating its implications to stakeholders.

Table 1: CEO-to-Median Employee Pay Ratios – Russell 3000

View of Governance Influencers

Governance influencers such as proxy advisors and the CCGG largely agree that the CEO pay ratio does not provide meaningful information to investors to support Say on Pay voting.

ISS (U.S.) – The CEO pay ratio is displayed for informational purposes only and does not affect say-on-pay or director vote recommendations. [1]

Glass Lewis – CEO pay ratio is not a determinative factor in its voting recommendations, Glass Lewis added a statement that “the underlying data may help shareholders evaluate the rationale for certain executive pay decisions such as increases in fixed pay levels.” [2]

The Canadian Coalition for Good Governance (CCGG) – View that the CEO pay ratio distracts from other issues around compensation, noting that it lacks comparability. [3]

Global Developments Around CEO Pay Ratio

Globally, we are seeing diverging views around CEO pay ratio, with the US potentially scaling back disclosure rules and the UK seeing growing attention around the issue of executive vs. broader employee pay levels.

United States

In June, the Securities and Exchange Commission (SEC) held a roundtable on executive compensation disclosure requirements. The CEO pay ratio disclosure requirement was a key topic of discussion and participants generally agreed that complying with disclosure requirements is too costly for organizations when weighting the limited benefit of this data to investors (refer to this article from GECN partner firm, Farient Advisors). Considering the consensus on this topic, it is likely that we will see the U.S. disclosure requirement removed in the future.

United Kingdom

In the UK, we have also observed pressure from policymakers, investors, and the public to ensure that executive pay increases do not outpace increases for broader employees. For example, advocacy groups like the High Pay Centre have been vocal about the need for more equitable pay structures.

Key Takeaways

Given the complexities inherent in externally comparing CEO pay ratios, there is limited benefit in implementing CEO pay ratio disclosure requirements similar to those in the US and UK within Canada. However, CEO pay ratios, and broader vertical benchmarking can serve as valuable instruments for HRCs, supplementing traditional horizontal benchmarking methods. These tools aid in assessing the suitability of CEO compensation over time, especially in light of increasing global pay transparency and the expanded oversight role of the HRC in ensuring equitable remuneration practices.

In our blog on Ontario’s New Pay Transparency Legislation, we discuss other considerations for addressing fair pay, including having a clearly defined compensation philosophy, adopting a robust job architecture framework, maintaining market competitiveness, and conducting regular fair pay risk assessments. Incorporating pay ratios, findings of gender pay reviews, and broader workforce compensation trends into a human capital dashboard can support the HRC in fulfilling their oversight role. As expectations around pay transparency continue to evolve, equipping the HRC with the right tools and insights can support thoughtful and well-informed oversight of executive compensation.

[1] ISS’ view on CEO pay ratio

[2] Glass Lewis’ view on CEO pay ratio

[3] CCGG view on CEO pay ratio

About The Author

Taylor Richards, Principal

Taylor is a Principal at Southlea Group with 9 years of experience.

Prior to joining Southlea Group, she worked at Willis Towers Watson for over 5 years, managing projects for boards and senior management teams related to effective executive and broad-based compensation program design and governance.

She has experience supporting companies with a variety of compensation related initiatives, including total rewards philosophy and peer group development, competitive benchmarking of board, executive, and broad-based pay, compensation structure development, short- and long-term incentive plan design, and governance of compensation programs.

Taylor has experience supporting public and private companies across many sectors, with a focus on financial services and asset management.

Taylor graduated with an Honours Business Administration degree from the Ivey Business School at The University of Western Ontario, and a Bachelor of Arts degree with an Honours Specialization in Psychology from The University of Western Ontario.