The following memorandum summarizes the say on pay voting results in Canada (among the TSX Composite companies) and the U.S. (among the S&P 500 companies) based on results released by May 15, 2026. The data were collected by ESGAUGE, a data analytics firm.

Canada Results

At this point in the AGM cycle, 117 Canadian companies have reported their say on pay results for 2026. Early indications suggest that voting results are becoming more dispersed than last year, as summarized in Table 1.

Table 1 – Canada say on pay results

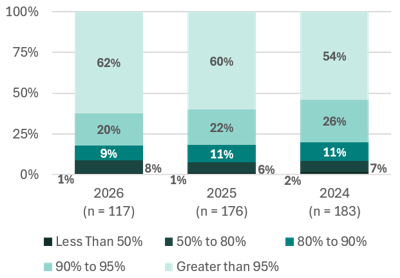

Chart 1 – Distribution of Canada say on pay results

As shown in Chart 1, as of mid-May 2026, 62% of companies received over 95% support, 20% received 90% to 95% support, 9% received 80% to 90% support, 8% received 50% to 80% support, and one company failed.

Companies trigger proxy advisors ISS and Glass Lewis’ board responsiveness evaluation when their say on pay support levels fall below 80%. Issuers’ responses generally should include engagement efforts, shareholder feedback, actions taken, and rationale for pay decisions. Although the 2026 proxy season is still underway, a higher proportion of companies have received less than 80% support than in the full year last year.

Of the reporting companies, 89% reported results that changed by less than 10 percentage points year over year.

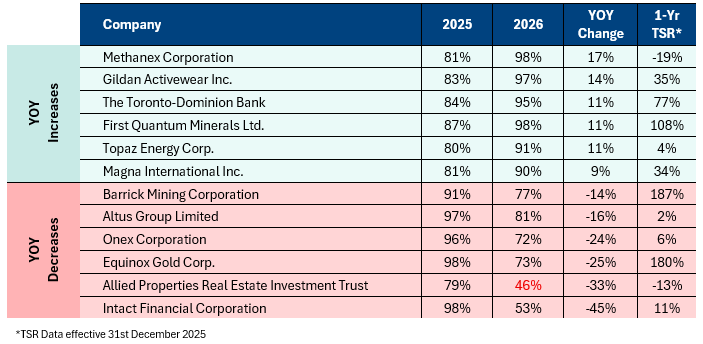

Table 2 – Biggest year-over-year changes in say on pay voting results

So far this year, we have observed several cases of much larger year‑over‑year gaps in voting results. Intact Financial is one example of shareholder frustration with one-time equity awards. In this case, special performance stock options (in addition to annual equity grants) contributed to the CEO’s disclosed 65% year-over-year pay increase, despite the company’s lackluster performance relative to peers. Both ISS and Glass Lewis issued AGAINST recommendations on Intact’s say on pay vote, disagreeing with Intact’s cited need for CEO retention given the value of outstanding equity awards (including the unvested value of the last special grant of stock options in 2021), and citing concerns about the misalignment of CEO pay and performance.

The only company that has failed a say on pay vote year to date is Allied Properties REIT, which received an AGAINST recommendation from ISS but a FOR from Glass Lewis. ISS identified a misalignment between pay and performance both in its quantitative and qualitative assessments, partly because ISS used the executive chair’s compensation for evaluation in years when it was significantly higher than the CEO’s. In addition, following a sub‑80% vote result last year, the company’s disclosure around shareholder feedback from engagement meetings, the board’s review process, and specific compensation design changes was considered insufficient.

U.S. Results

In the U.S., among the 272 S&P 500 companies that had reported as of May 15, 2026, the average level of support is slightly higher than last year’s average (see Table 3).

Table 3 – U.S. say on pay results

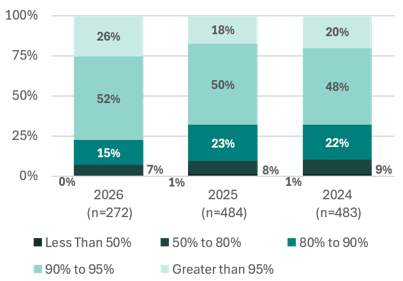

Chart 2 – Distribution of U.S. say on pay results

As illustrated in Chart 2, the percentage of companies garnering more than 95% shareholder support climbed from 18% to 26%, and the overall proportion of companies receiving over 80% support also increased slightly. In addition, only one company has failed the say-on-pay vote year to date, compared with seven in total last year.

Evolving Proxy Advisor Models and Influence

The proxy advisor landscape has shifted significantly over the past year. In early 2025, following President Trump’s executive order on DEI, both ISS and Glass Lewis softened their policy guidelines on director diversity. Later in the fall, Glass Lewis announced a major transition from a single-policy research model to tailored voting perspectives beginning in 2027. In December 2025, President Trump issued an executive order targeting ISS and Glass Lewis, aiming to reduce their influence. At the same time, large institutions such as JPMorgan and Wells Fargo publicly announced that they would discontinue the use of proxy advisory services and instead rely on internal systems for policy application and proxy voting.

Against this backdrop of evolving proxy advisor practices, this year we have observed several cases where FOR or AGAINST recommendations from proxy advisors no longer correlate as strongly with shareholder support for say‑on‑pay as in prior years. As proxy advisor influence shifts, the uncertainty of voting outcomes has increased. As a result, companies must engage directly with their shareholders to understand their voting guidelines, rationale, and expectations. On the other hand, issuers are also moving away from uniform or standardized practices shaped by proxy advisors and are instead pursuing innovative pay design solutions tailored to their unique strategic needs.

About The Author

Anqi Xu, Consultant

Anqi is a Consultant at Southlea Group, where she leads the Compensation Governance team.

Before joining Southlea Group, she served as Associate Vice President at ISS, a global proxy advisory firm, where she produced independent shareholder meeting research reports with voting recommendations for institutional investors. She also acted as the Canadian research team’s Environmental & Social (E&S) lead, specializing in E&S shareholder proposals.

Anqi has also held the position of Vice President at Kingsdale Advisors, a leading Canadian strategic advisory firm, where she advised boards and committees on complex corporate governance matters, including proxy contests and mergers and acquisitions. She provided strategic advice to public companies on executive compensation and was instrumental in several successful Say on Pay turnarounds.

Anqi brings extensive experience in assessing executive compensation frameworks and facilitating effective disclosure for publicly traded companies, particularly those listed on the S&P/TSX Composite Index, across multiple industries.

Anqi holds a Bachelor of Arts in Economics and Art History from the University of California, Los Angeles (UCLA), and a Master of Financial Accountability from York University. She is also a Chartered Financial Analyst (CFA) charter holder.