Key Takeaways

- *New analysis this year* The overall riskiness of a pay package is primarily driven by the degree of performance exposure and the longevity of the pay elements

- The riskiness of CEO total direct compensation (salary plus short- and long-term incentives) has decreased overtime as companies have moved away from stock options to a higher weight on performance share units and restricted share units, while total direct compensation continues to increase

- In addition, the time needed to fully realize compensation is getting shorter (e.g., ~2.4 years) which may not be considered truly long-term and aligned with the risk tails associated with strategic decisions

- Conversely, European companies are looking at ways to increase the overall riskiness of the pay package

- Continued pressures on pay given inflation, tight labour markets and increasing global competition with 50th percentile actual total direct compensation for CEOs up 12% and CFOs up 3% (for the same CEO / CFO incumbents year-over-year). Salaries at the 50th percentile were up by 7 to 9% for CEOs and CFOs while actual bonuses (as a percentage of target) were down to 1.2x target from 1.6x target last year

- Performance share units continue to form a greater proportion of the long-term incentive mix. The weighting on stock options continues to decrease, but they remain highly prevalent used by over 60% of the S&P/TSX 60

- Relative TSR continues to form the majority weighting of performance share unit plans. More than 75% of companies use more than one measure suggesting a combination of relative TSR and another measure(s), increasingly ESG-related

- Say on pay average levels of support continue to increase with only three failures in 2023 (same as 2022)

Performance Context

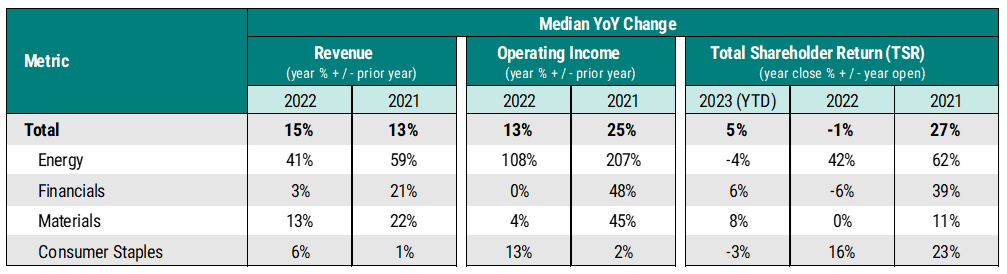

In 2022, we saw a more challenging performance year with lower growth in operating income and challenging total shareholder returns (TSR). We continue to see significant differences by industry, with energy and consumer staples outpacing materials and financials (refer to Table 1). As we look forward to 2023, we anticipate more challenging performance conditions given higher inflation and interest rates, lower growth expectations and overall geopolitical uncertainty. More modest performance outcomes – including relatively flat TSR – may raise questions on the pay-for-performance relationship.

Table 1: 2021/2022 Performance Summary

Data effective date: June 15, 2023

Pay Longevity *New*

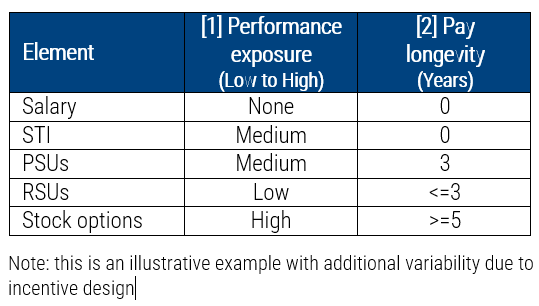

As we see changes in how pay is delivered, particularly the shift away from stock options to performance share units (PSUs), we wanted to assess how Canadian executive compensation plans address the uncertainty embedded into incentive plans. The overall “riskiness” of a pay package is primarily driven by the degree of performance exposure (e.g., risk of not receiving target pay) and the longevity of the pay elements (e.g., period needed for total awarded compensation to become realizable).

In this graph, we show the general relationship between the performance exposure and pay longevity of a typical executive compensation package consisting of the following elements:

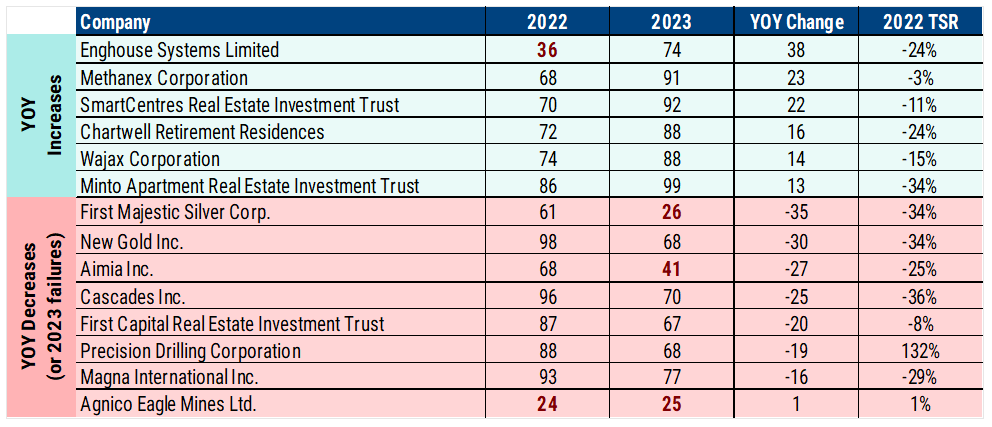

Table 2 – Biggest year-over-year changes in say on pay voting results

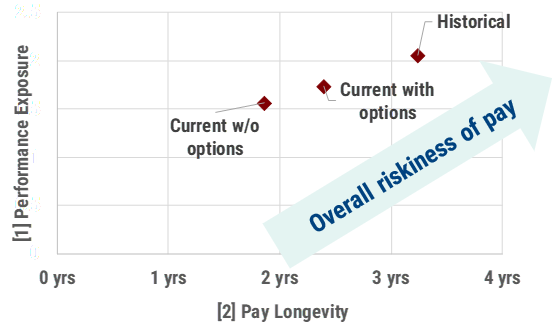

As programs shifted from a historical mix of 50% stock options and 50% PSUs to the current mix of 75% PSUs and 25% RSUs or 50% PSUs, 25% options and 25% RSUs, the riskiness of the pay package has decreased while total pay has increased.

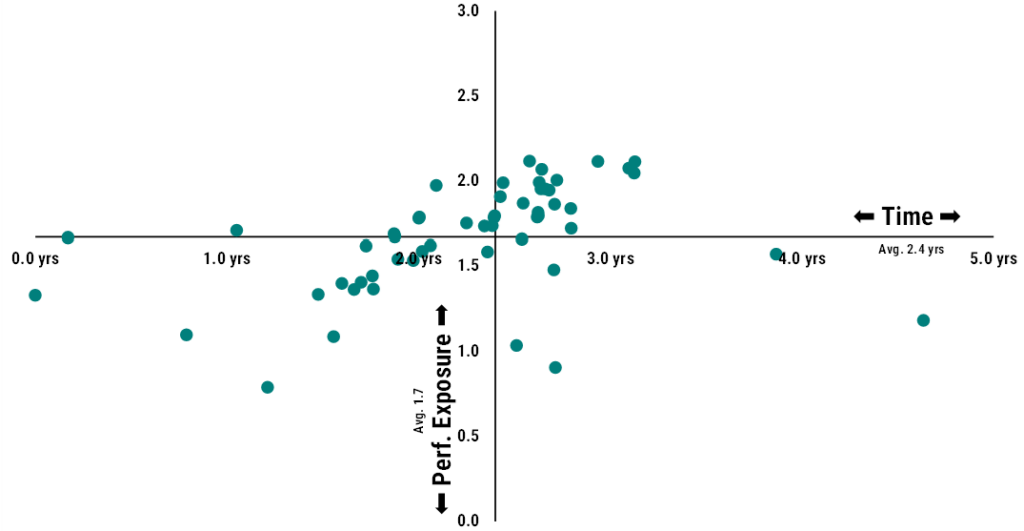

As illustrated in Chart 1, most of the S&P/TSX 60 companies are clustered in the middle with an average longevity of 2.4 years. This means a CEO fully realizes their total pay in only 2.4 years which may not reinforce a long-term orientation and/or align with the risk tail of their strategic decisions. The longevity of CEO pay packages in Europe continues to increase through longer-vesting performance equity and a greater emphasis on long v. short-term incentives.

Chart 1: Pay Longevity

Market Compensation Trends

The following compensation trends are based on the same incumbent through 2021 and 2022, and reflect actual compensation disclosed in 2022 and 2023 proxy circulars, including actual salaries, actual/target bonuses and long-term incentive grants (on an as-reported currency basis, as disclosed).

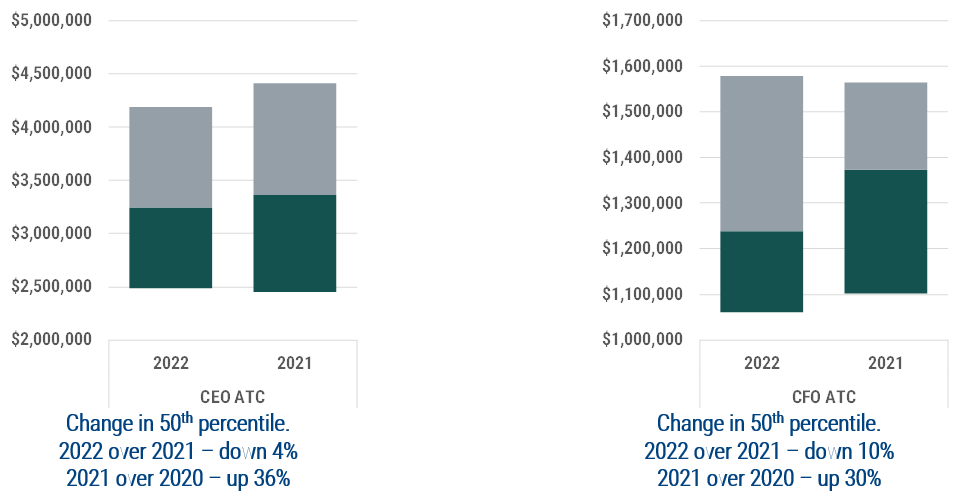

Chart 2: 2021 and 2022 Salaries

The median CEO salary in 2022 increased by 7% to $1.187M (from $1.114M in 2021). The median CFO salary increased by 9% to $642,000.

Chart 3: 2021 and 2022 Actual Total Cash

Median actual total cash (ATC) decreased by 4% for CEOs and 10% for CFOs in 2022. The median actual bonus as a percentage of target bonus for CEOs decreased to 1.17x target in 2022 from 1.61x target in 2021.

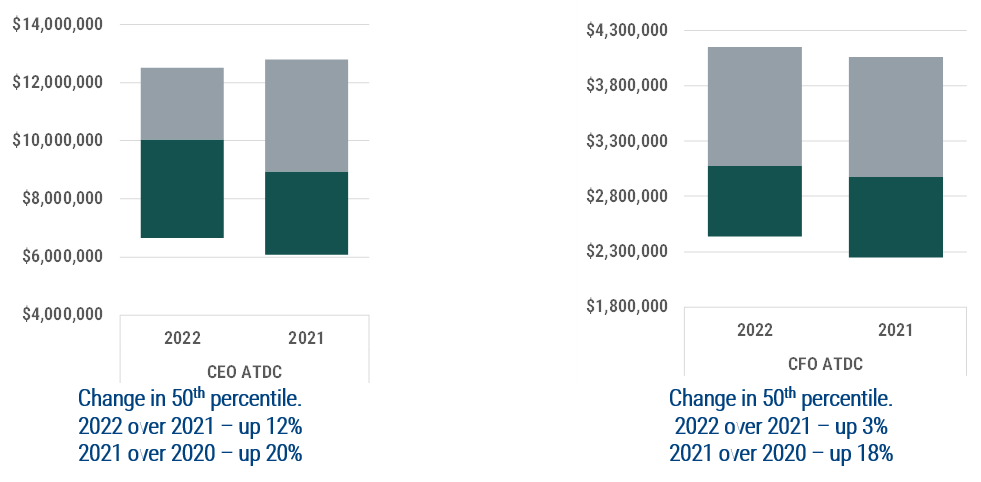

Chart 4: 2021 and 2022 Actual Total Direct Compensation

Median actual total direct compensation (ATDC) increased by 12% for CEOs and 3% for CFOs in 2022, primarily driven by higher salaries and long-term incentive grants. The median grant value of long-term incentives increased to 533% of salary from 485% for CEOs and remained flat at ~270% of salary for CFOs.

We observe a relationship between company size – in terms of market capitalization – and CEO ATDC (i.e., larger companies pay more than smaller companies); an important consideration when interpreting these findings.

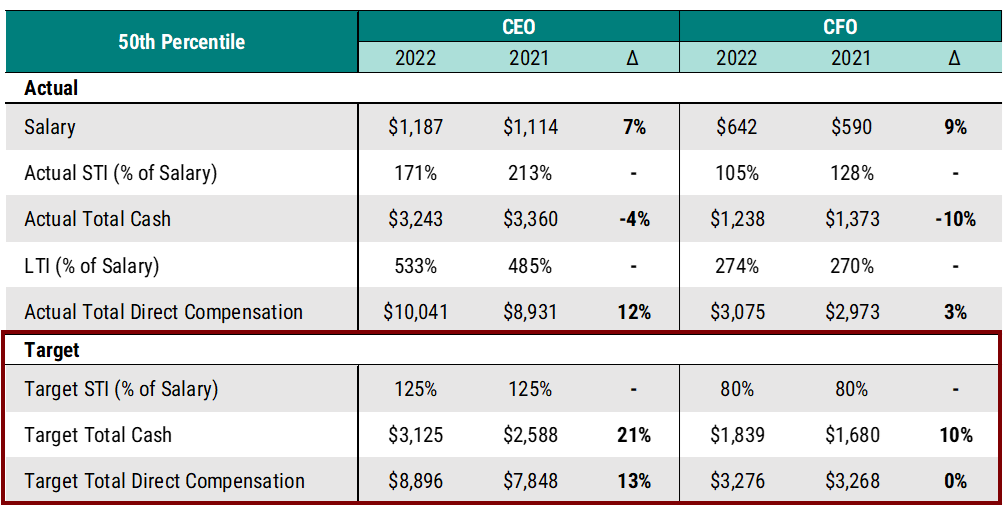

Table 2: Year-Over-Year Changes in 50th Percentile Pay

As illustrated in Table 2, target total direct compensation levels year-over-year, where disclosed, were up 13% for CEOs and flat for CFOs.

Table 3: Significant Year-Over-Year Changes in CEO ATDC

There were several large year-over-year compensation changes among CEOs, primarily due to changes in LTI grants and, in many cases, one-time or situational LTI awards.

Gender Distribution

We also reviewed the gender distribution of the CEOs and CFOs within the S&P TSX 60 and found only one female CEO (new in 2022) and eight female CFOs (up from seven in 2021). Given the limited number of female CEOs and CFOs, we were unable to review the compensation data by gender. Amongst all named executive officers (NEOs), we saw a slight increase in the number of female NEOs from 23 to 34 (8 to 11%) of all NEOs.

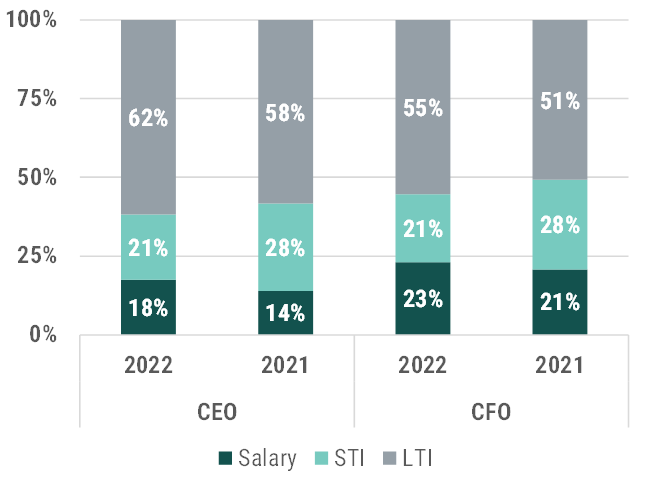

Chart 5: CEO and CFO Pay Mix

In terms of overall CEO and CFO pay mix, Chart 5 shows that salary (or fixed pay) represented less than 20% of actual total direct compensation.

Actual short-term incentives (STI) represented approximately 1.2x salary for CEOs and 1.0x for CFOs and comprised a lower proportion of total pay relative to 2021 due to lower bonuses.

Companies continued to put a majority weighting on long-term incentives (LTI). This captures the value of the LTI at grant, but the actual value realized can vary significantly, reinforcing the importance of ensuring this portion of compensation is designed appropriately and aligned with strategy / shareholder interests.

Short-Term Incentives (STI)

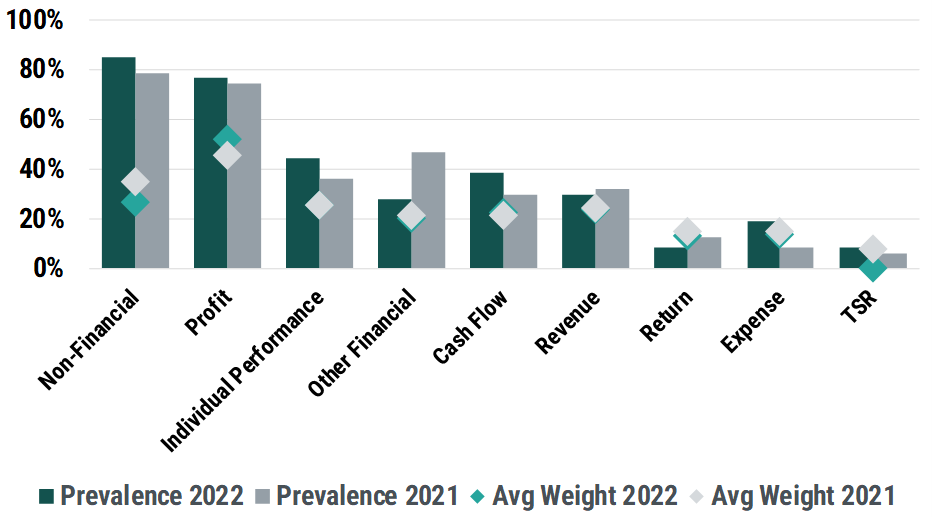

Chart 6 summarizes the prevalence and mix of performance measures within the STI plan. Non-financial and profit-based measures were the most common, with non-financial measures weighted at about 30% and profit measures at about 50% of the overall STI score. The use of ESG-related measures continued to evolve and more details can be found in this report. Modest changes year-over-year, with the average weight on profit measures increases, offset by the average weight on non-financial measures and TSR decreasing.

Chart 6: Prevalence and Mix of STI Performance Measures

Long-Term Incentives (LTI)

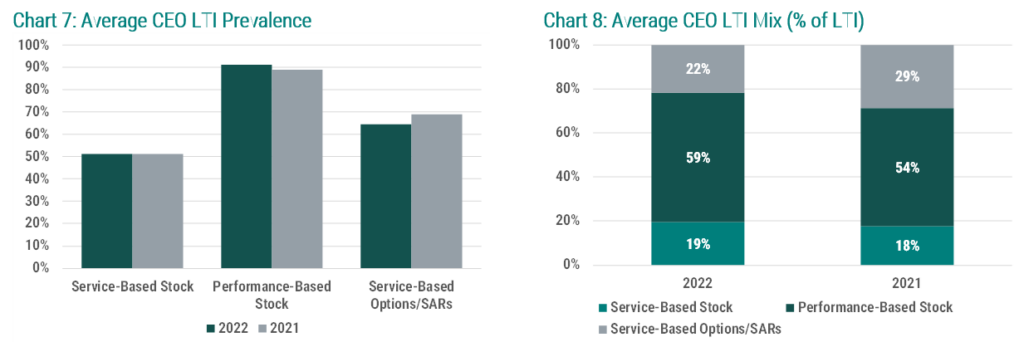

Chart 7 (on the left) summarizes the prevalence of the long-term incentive vehicles granted to the CEO in 2022 and 2021 and Chart 8 (on the right) summarizes the average mix of long-term incentives granted to CEOs over the same period. There was a slight increase in the

prevalence and weighting on PSUs in 2022. While the prevalence of stock options remained the same (about 65%), their average weighting in the overall LTI portfolio dropped to 22%. A number of companies that had higher weightings on stock options reduced their weighting, resulting in a lower average mix of 20-30%.

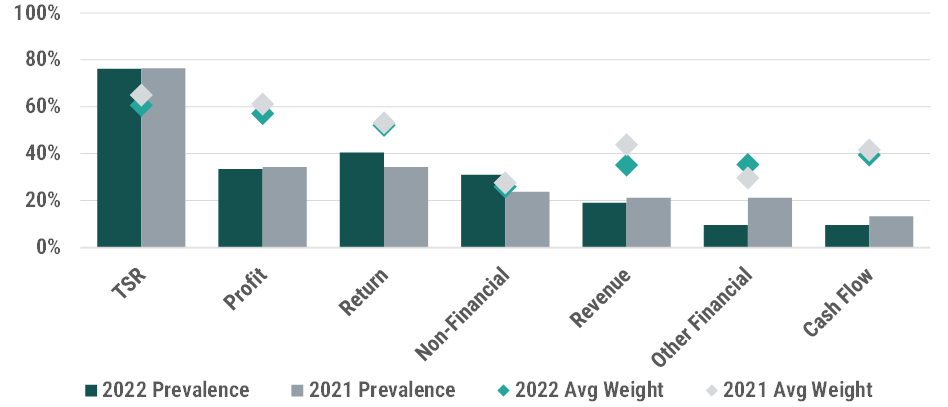

Chart 9 summarizes the prevalence and mix of performance measures in PSU plans. We saw some shifts in the types of measures, but average weightings remained generally consistent. TSR remained the most common metric with an average weighting of approximately 60%. Given the increasing use of PSUs and relative TSR, there is more pressure on companies to get this component right, including participation, selection of the relative TSR comparison (market index or peer group) and the performance range calibration.

Chart 9: Prevalence and Mix of PSU Performance Measures

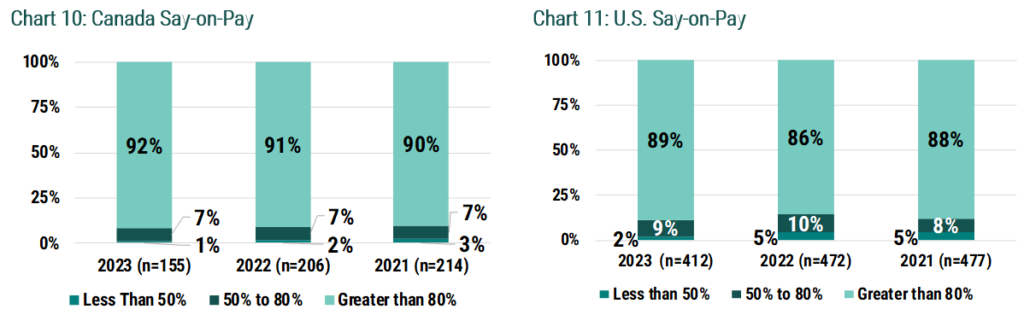

Say-On-Pay

Charts 10 & 11 summarize the say-on-pay results (as of June 15, 2023) for Canada (left) and the U.S. (right). In Canada, the average say-on-pay vote remains strong at 92% in 2023 (compared to 91% in 2022 and 2021). In the U.S., the average score has increased slightly to 89% from 87% and 88% in 2022 and 2021, respectively. Refer to our earlier memo for further details.

For most companies, there is little year-over-year change in the reported say-on-pay results and Table 4 highlights the most significant year-over-year increases and decreases. There were three failures in 2022, and, as of June 15, there have also been three failures in 2023 with Agnico Eagle failing in both years, largely due to special transaction-related cash bonuses.

Table 4: Significant Year-Over-Year Changes in Say-on-Pay Support

About This Author

Ryan Resch, Senior Partner

Ryan is a founder and Senior Partner of Southlea, a GECN Group company. He has over 20 years of experience consulting complex organizations across North America on executive and broad-based compensation including related governance considerations. He is often the named executive compensation consultant representing either the human resources committee and/or management. Prior to forming Southlea, he worked in Willis Towers Watson’s Toronto and Vancouver offices leading many of the practice’s large client relationships.

He leverages this expertise to bring stakeholders together and drive meaningful change aligned with key business and talent priorities. He is known for providing fresh and innovative thinking with his most recent research focused on connecting environmental, social and governance (ESG) with people and pay programs.